More questions than answers...

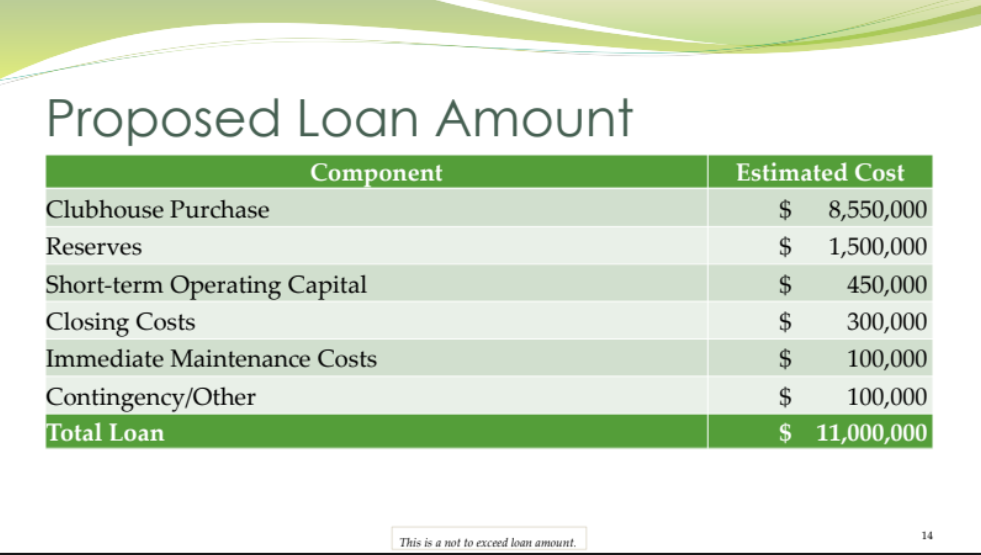

At the August 12 Townhall, the clubhouse acquisition committee presented a proposal to homeowners to purchasing the clubhouse and combining operations of the HOA with the Clubhouse. Now It is up to us to choose whether to proceed with an accelerated, proactive offer to purchase the clubhouse from LEN-South Shore bay with 30 year fixed rate financing on $8.550,000 purchase price with an $2,450,000 of proposed un-itemized additional costs. (Would you agree to a home mortgage where unspecified add on costs are 29% over the purchase price?).

Rushed timing - Why now? Homeowners had just 12 days to evaluate the largest purchase we'll likely ever make and ALL homeowners must participate in the financing (even those who wish to avoid interest and pay upfront). And the August 27 special meeting agenda format provided no opportunity to ask questions and no time to get answers. Why was this the first time ever that our HOA had a public, proxy-only ballot required for a membership meeting? (Past ballots were private, with homeowner's address on outside of envelope for identity verification.)

An affirmative vote would also combine the Medley HOA with all clubhouse operations under the current board of directors and Castle group “without further membership vote" per the "Limited Proxy Membership Meeting" mailed to us.

After careful consideration, Medley Members' team advises voting NO and encourage others to do the same. Here are some of the reasons.

1. Interest Rate - The interest rate proposed is 6%. However, JP Morgan and even the Fed just stated that the Federal Reserve is expected to lower interest rates at their September meeting and possibly even further this year. A reduction of just one point could reduce financing costs by up to $3 million.

2. Timing - Per the Club Plan, LEN has up to April 2027 to offer the Clubhouse for sale to us. Homeowners are told we should proactively make an offer because the sale price of the clubhouse specified in the Club Plan will increase next year. However, it is also true that a lower interest rates as well pruning the $2.45 million in add-ons could offset that. We should not approve a loan amount without first seeing itemized justification and expenses of the additional costs.

3. Club ‘s operating costs - Once purchased, we would be responsible for all Club operating costs. However, there was no prospective Club financial statement provided to homeowners despite the committee having been provided a recent club P&L financial statement. (It is never a responsible business practice to borrow money to purchase a business without a business plan. The board will form another committee for that but we will already have been committed by then.) Moreover, our $170,000 Special Assessment already allocated $50,000 for "Clubhouse Purchase evaluation"(see here). Where did that money go?

4. Potential Alternatives -The board has a duty to present ALL alternatives to HOA members. LEN has reportedly approached the board with an offer to continue operations as is, which would not require us to take on any debt. If so, let’s compare and vote on ALL the options. We may even have up to 18 months to decide. Given many homeowners here are on fixed incomes, it seems irresponsible to force them into any monthly price increase without a vote on this option if available. And tacking on ~$11,000 to the sale of every home here hurts all of us.

5. Leverage? - A 2023 lawsuit (Avatar Properties Inc. v. Gundel) determined that it was improper for the nonprofit Solivita Homeowners Association to pay for the profits of the clubhouse’s owner. The court ruled that assessments used to fund the club's operations, which included a significant profit component, were improper under state law. To date, we homeowners have not heard the board, our HOA attorney or committee member indicate whether this legal precedent might benefit to us.. We homeowners we have been paying $50 a month to LEN as a profit over the years. (That has accumulated to approximately $2.5 million. ). Might there be an opportunity for a savvy outside attorney to leverage that to negotiate prepaid reserves ? Or even just to open LEN’s books? It’s worth investigating.

6 Conflicts Check - With millions of dollars in play for this HOA loan, all involved parties should first attest to having no conflicts of interest with the proposed lender (e.g. Popular bank) or any future servicing vendor (TownSq, Castle Group, etc.). Conflict of interest reporting is standard practice for nonprofit board members, attorneys, association managers (CAMs) , committee members , etc. (See FL 720.3033(6), 468.335) Homeowners should have this information before a vote.

In summary, on or before August 27, we recommend voting “No, not in favor” to authorizing an $11 million dollar loan until such time as the items above are investigated and presented to homeowners. There will be an HOA member vote opportunity at our October 14 Annual Meeting where this topic could considered along with its impact to the overall budget.

--Already voted but change your mind? Per FL law, you can submit an updated proxy dated with time before/at the meeting to replace old one per 720.306(8)(a) which specifies that a proxy is "revocable ..by the person who executes it."

Sincerely,

Medley Members

Medley Members

Reminders for our HOA officers:

Nonprofit board members are bound by Florida statues of fiduciary responsibilities and duty of care. If informed of anything that conflicts with professional advice you may have received, §618.0830 (3) indicates you must investigate or are not acting in "good faith." (That might even void your liability protection.)

COMMENTS OR CORRECTIONS ARE WELCOMED BELOW

- Please be polite and do not use individual's names. (If necessary, use titles or initials instead)

- You can use our comment boxes as 'guest' to provide feedback anonymously on MedleyMembers.net. (No Facebook bullies here! 😅)

- If you are posting a correction, cite the source document, a link to the location and/or the quote, otherwise it's just an opinion.